Confidential Broker Opinion of Value

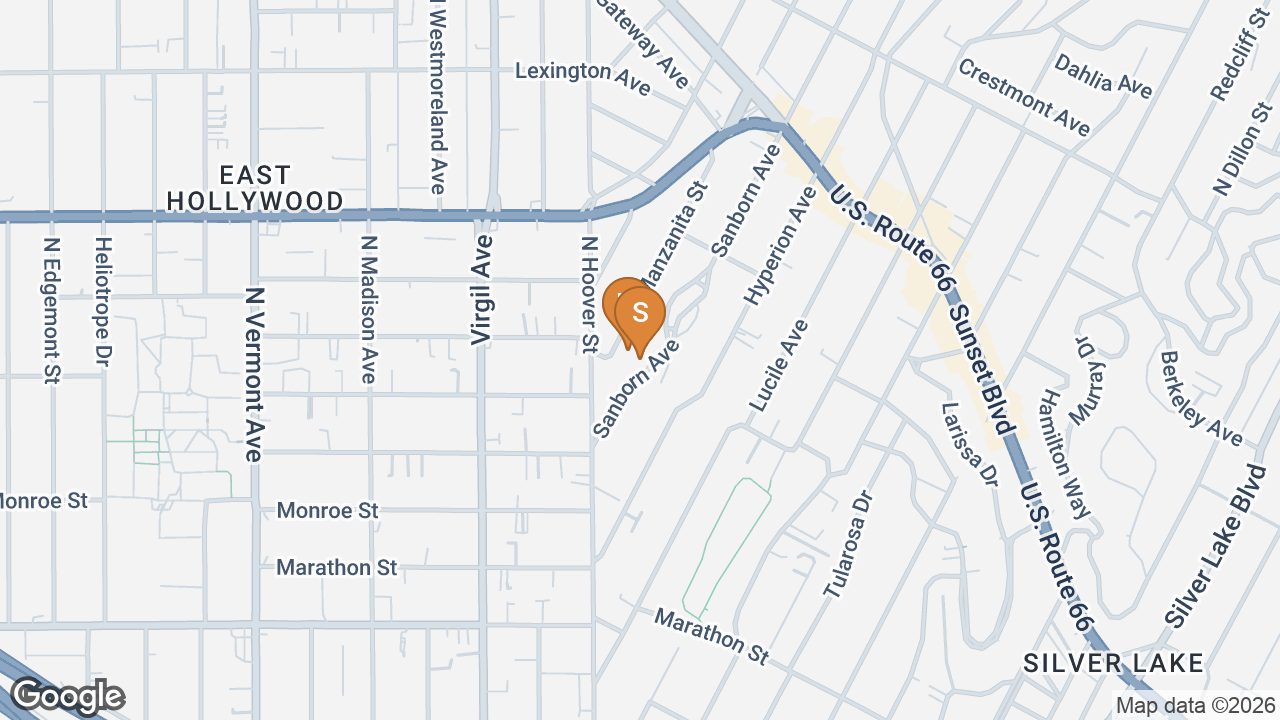

904 Manzanita St

& 905 Sanborn Ave

& 905 Sanborn Ave

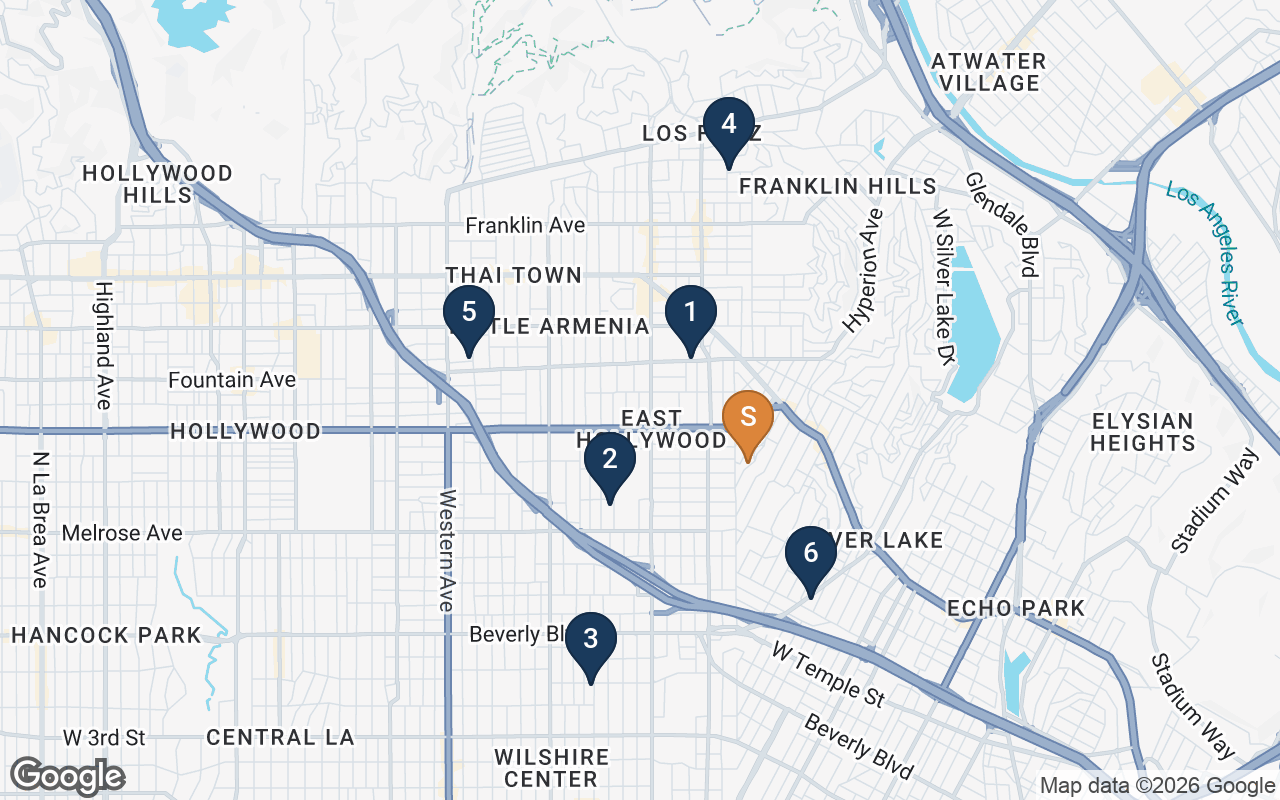

Silver Lake · Sunset Junction · Los Angeles, CA 90029

11Units · 2 Parcels

5,977Building SF

1916 · 1927Years Built

11,109Combined Lot SF

Glen Scher

Senior Managing Director Investments

Marcus & Millichap · LAAA Team

Marcus & Millichap · LAAA Team

Filip Niculete

Senior Managing Director Investments

Marcus & Millichap · LAAA Team

Marcus & Millichap · LAAA Team

Jon Adams

Real Estate Investment Advisor

Carolwood Estates

Carolwood Estates

Prepared Exclusively for Juan Martinez

July 2026